You probably know about the initial enrollment period for Medicare. It starts three months before your 65th birthday, includes your birthday month, and continues for three months after your birthday month. But did you know that you can actually sign up for premium-free Medicare Part A “any time during or after your Initial Enrollment Period starts” and that the coverage is backdated if you sign up after you turn 65? Here’s what the Medicare.gov website says:

- If you sign up for Part A during the first three months of your Initial Enrollment Period, your coverage will start the first day of the month you turn 65.

- If your birthday is on the first of the month, your coverage will start the first of the prior month.

And, if you sign up for Medicare Part A within six months of your 65th birthday, your coverage will still start on the first day of your birthday month (or the first of the prior month if your birthday is on the first).

If you sign up after that, the effective date of Medicare Part A coverage is retroactive six months from when you sign up.

Why is this important? Because a lot of people postpone their Medicare coverage so they can stay on a group health plan and continue to contribute to a Health Savings Account. And that’s fine, but if you market to group clients, or if you have Medicare-eligible clients who are working past age 65, you may want to inform them that they will need to stop contributing to the Health Savings Account six months before they plan to sign up for Medicare. If they don’t plan ahead and they contribute more than the pro-rated amount during the year they sign up for Medicare, they may have to back some of the funds out of the HSA to avoid taxes and a penalty.

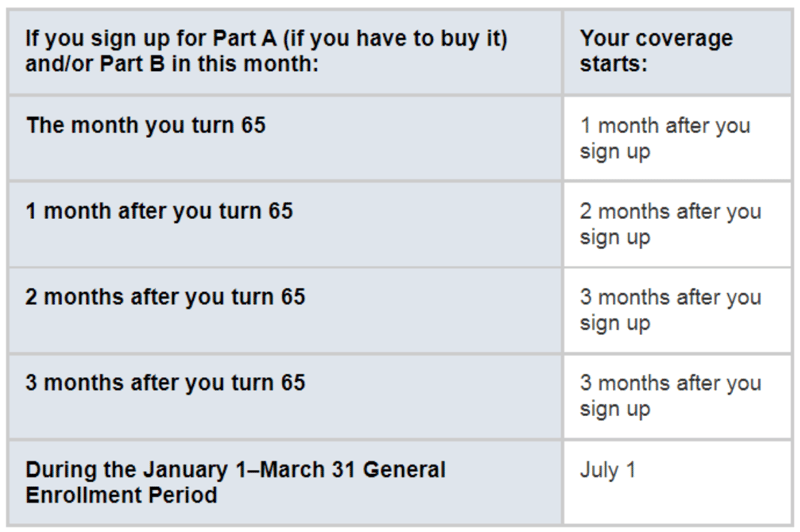

Keep in mind that the retroactive Part A coverage only applies to premium-free Part A. For those who have to pay for their Medicare Part A benefits, the effective date is the same as it would be for Part B. Here’s a chart from the Medicare.gov web page explaining that: