A lot of emphasis has been placed on the Affordable Care Act’s premium tax credits over the past couple years—and rightly so. The Advanced Premium Tax Credit (APTC) makes it possible for millions of Americans to purchase health insurance; without the financial assistance, many would likely remain uninsured.

There is another type of financial assistance, though, that gets a lot less fanfare than the APTC: cost-sharing subsidies. While you may have learned about the subsidies when the law was first passed and are likely guiding your lower-income clients to subsidized plans, we thought you might benefit from a quick review of how the subsidies work, in turn enabling you to better explain them to your clients.

Purpose

To begin with, we need to understand the purpose of the cost-sharing subsidies. Quite simply, they’re intended to help people pay their out-of-pocket health insurance costs. While the premium tax credits help reduce the number of people who are uninsured, the cost-sharing subsidies help reduce the number of people who are underinsured, meaning their total exposure is lowered. This decreases the likelihood that someone—particularly low income individuals and families—with health insurance will have to file for bankruptcy.

Eligibility

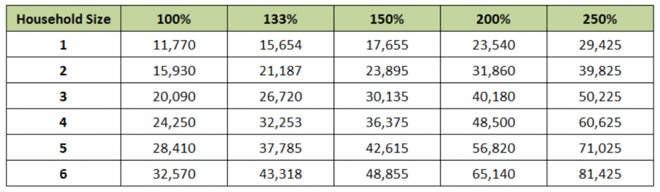

While the premium tax credits are for people with incomes up to 400% of the federal poverty level (FPL) who don’t have access to other minimum essential coverage, the cost-sharing subsidies are for those people with incomes up to 250% of the FPL. The FPL figures for 2016 won’t be released until the third week in January, but the 2015 federal poverty levels are shown below.

2015 Federal Poverty Level (48 Contiguous States and DC)

Source: http://aspe.hhs.gov/2015-poverty-guidelines

Those who wish to take advantage of the cost-sharing subsidies, however, are required to buy coverage in the silver level of the individual marketplace. The premium tax credit, as you know, is calculated based on the benchmark silver-level plan but can be used to purchase coverage in any metallic tier. The cost-sharing subsidies, on the other hand, are only offered in the silver level.

Higher AV, Lower OOP

So how, exactly, do the cost-sharing subsidies lower an individual’s exposure to high claims costs? In two ways: by increasing the actuarial value and lowering the maximum out-of-pocket limit.

Actuarial Value: The actuarial value (AV) of a plan is a measure of the total amount of claims cost a plan pays, on average, for a large population. Silver plans typically have an actuarial value of 70%, but the cost-sharing subsidies increase the AV to 73%, 87%, or 94% depending on the household income. The benefit of an increased actuarial value is that the plan may have a lower calendar year deductible or lower up-front copayments.

Out-of-Pocket: Cost-sharing subsidies also reduce the out-of-pocket (OOP) limit of a plan. In 2016, the maximum out-of-pocket for those with single coverage is $6,850. Individuals with cost-sharing subsidies qualify for an OOP-max reduction, again determined by FPL.

- Those at between 200% and 250% of the FPL qualify for a 20% reduction.

- Those at between 100% and 200% of the FPL qualify for a reduction of more than 60%

In these examples, the out-of-pocket maximum is brought down to $5,480 or $2,283, respectively, depending on the household income.

Cost-Sharing Subsidies at a Glance

Your Clients Need Your Help

Your clients may have a little trouble understanding the cost-sharing subsidies, but that’s okay. Where they really need your guidance is in picking the right plan. Because the plans that qualify for a cost-sharing subsidy are just mixed in with all of the other plans that are quoted through Healthcare.gov, you’ll want to guide your client to a lower overall exposure. Anyone who tries to select a plan themselves, without the assistance of an agent, may wonder why some of the better plans are no more expensive than other plans with significantly higher exposure.

It’s also important to remind your clients that they need to keep the Marketplace informed about any change in their income or family status as it could affect their eligibility for both premium tax credits and cost-sharing subsidies.