Most of us didn’t grow up wanting to be insurance agents. Instead, the majority of insurance professionals found their way into the business by accident. There are a million stories, but what we’ve heard again and again from brokers across the country is that 1) they sort of stumbled into the industry, 2) now that they’re here, they really like it and don’t want to leave, and 3) they wish they had started when they were younger.

That brings up an interesting question: are you teaching your kids the business? And if not, why not?

There are all sorts of things that make health insurance an excellent career choice. Here are a few:

- Great income potential – It really is unlimited. Someone who is motivated and works hard can make a good living relatively quickly and a lot of money over time.

- No specific education requirements – While many agents have a college degree, and while that may be necessary to land a job at a big firm, there are no degree requirements to sit for the licensing exam or to start your own agency. That means that someone could get started right out of high school.

- Flexibility – Independent agents can set their own hours, sell insurance part-time while working a full-time job or going to school, and work from home. It really does provide a lot of lifestyle flexibility.

With all of those things going for it, who wouldn’t want to be an insurance agent? If you agree, that’s all the more reason to introduce your children to the business. It could set them up for success very early in life.

Get Them Started Early

Here’s an idea. What if you began teaching your kids about insurance as they enter high school? It wouldn’t take long for them to understand the need for health coverage, be able to differentiate between a deductible and copayments (something many of our clients still can’t do), and choose the plan that provides the best protection at the lowest price. You could teach them how to run quotes, enter those quotes on a spreadsheet, and put together a proposal. They could even help you file papers and perform other tasks around the office. In other words, you could train them the same way you would a new agent or account manager, and by the time they graduate from high school, they would likely know as much as many seasoned insurance professionals.

If your son or daughter were to take the exam and get his or her insurance license at age 18, just think how far ahead he or she would be. Your child could start selling business, a little at a time. Perhaps you could pass along a lead here or there, easy ones at first just so they can get their feet wet. Over time, your son or daughter could have a nice income that could help pay for college.

Income Potential

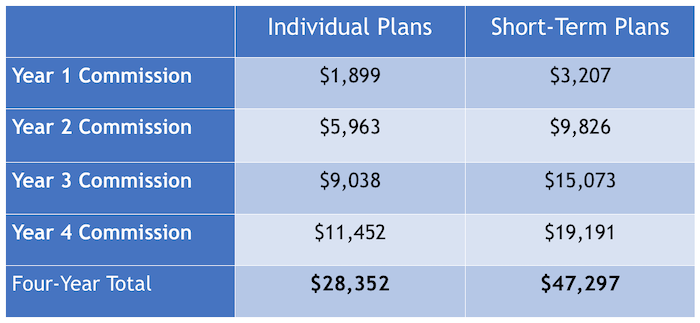

To illustrate, what if they sold just one individual or short-term policy per month (and three per month during the summer) while earning a four-year college degree? If they were to retain just 75% of the business annually, here’s what the income stream might look like:

Our assumptions in this calculation are that the average individual premium is $450 per month and pays 5% commission. The average short-term plan is $190 and pays 20% commission. We also assume that your child(ren) will lose 2% of their business per month for a total of 24% per year and that every policy they sell is to an individual with no spouse or dependents.

Obviously, each of these assumptions is fairly conservative. Prices vary by carrier and by location, and many of today’s individual health plans are well over $450 per month and usually increase from year to year. Many earn more than 5% commission, and the drop-off rate would probably be less than 20% per year and certainly wouldn’t start right away. And, of course, many people buy coverage as a family and purchase ancillary and supplemental coverage, which could increase the potential income substantially.

A Great Fallback Plan

Our goal in this calculation is simply to show a conservative estimate of what is possible for a young adult who dabbles in health insurance in his or her spare time. Someone who focuses and tries to sell more almost certainly will, and the hope in getting your children started at an early age is that he or she could make some money while determining whether or not a career in health insurance makes sense. Even if the answer ends up being no, they’ll learn the business and will have a great fallback plan.

One other nice thing about teaching your children the business of health insurance, if they end up liking it, is that you will have a succession plan. If you’d like to retire one of these days, instead of selling your business or simply letting it dissolve, you will have someone to pass it on to. Who better than your own children?