If you’re a fan of Health Savings Accounts, you’ve probably experienced the frustration of trying to explain to clients why a High Deductible Health Plan with no up-front copayments is a MUCH better deal than a traditional plan with copayments for doctor visits and prescriptions, only to have the client ignore your advice and select the more costly plan that will not allow them to pay with tax-free dollars.

Why do people make decisions that aren’t in their best interest? Why do they insist on overpaying for their health insurance? Why are they willing to accept a higher deductible and higher out-of-pocket max just so they can go to the doctor for a predictable, flat-dollar fee?

The answer is simple: because they don’t understand insurance, and they have absolutely no idea how much a doctor visit actually costs.

That’s actually one of the goals of a consumer-directed health plan—to remove the copayments that shield people from the cost of health care so people will compare cost and quality and make better healthcare decisions. Unfortunately, nearly fifteen years after HSAs first hit the market, people are still scared of letting go of their precious copayments. They see these fixed costs as a security blanket; they appreciate the predictability of going to the doctor for $35 and are scared of having to pay the full contracted price.

So that begs the question, “how much does a doctor visit actually cost?” It’s an important question because, with this information, consumers can crunch the numbers and decide which plan makes the most sense for them; without knowing the cost of doctor visits, it’s more of a guess and they tend to stick with what they know instead of stepping outside their comfort zone.

Fortunately, there are some tools out there that can help. Some of these price transparency information is offered by the health carriers themselves. Unfortunately, that information is usually only available after an individual or employee signs up for coverage, which is not very helpful to someone who’s trying to decide whether or not to enroll in an HSA-qualified plan. Other tools are offered by third-party websites that aggregate information on the contracted prices for various carrier networks. These can provide more impartial data, but most people who use these services do so only when they need a big medical procedure and want to compare their options. Now, fortunately, some states are actually starting to make information available that can help consumers who want to know the approximate price they would pay without an up-front copayment, and this can be helpful during the decision-making process.

For instance, the Texas Department of Insurance recently launched a website available to the public called TexasHealthcareCosts.org. The site allows consumers to compare retail and discounted rates for a wide range of services across the state. The medical rates shown on the site are currently based on 2016 claims data and are shown as an average; consumers cannot use the site to compare costs between two different providers.

After entering his or her zip code, a consumer chooses from six different types of services:

- Inpatient Procedures

- Outpatient Procedures

- Imaging Services

- Pathology Services

- Office Visits

- Emergency Services

While all of this information can be beneficial, the cost of office visits can be particularly enlightening for someone trying to compare the out-of-pocket costs between a copay plan and an HSA-qualified plan. For most plans, all of the other services would be subject to the deductible, whether the plan has up-front copayments or not. For that reason, the main costs we should be interested in when comparing our options is the cost of office visits.

On a copay plan, of course, we know how much the cost of a primary care visit and a specialist visit will be since that amount is fixed. On an HSA-qualified plan, though, we have to pay the contracted rate for those services. That’s when we could use a site like TexasHealthcareCosts.org.

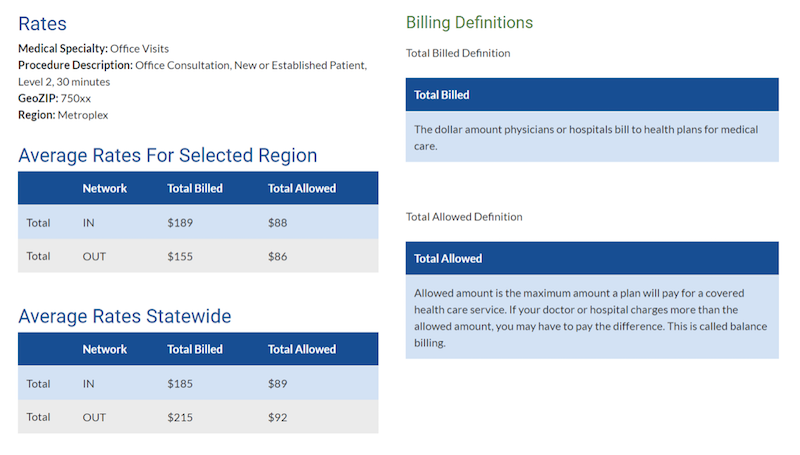

When the consumer selects “Office Visits” from the drop-down box, he or she can then choose from Women’s Health, Office Consultation, Office or Outpatient Visit, and Preventative Medicine Visit. If we select “Office Consultation, New or Established Patient, Level 2, 30 Minutes” in the Dallas area, here are the results:

In Dallas, the average primary care physician would charge $189 for a 30-minute visit but would contract with the insurer for $88, which is what the member would pay if he or she was on an HSA-compatible plan. Statewide, the average allowed amount is $89 for a 30-minute visit.

Put simply, if a couple tells you that they would prefer a copay plan because they have kids who have to go to the doctor a lot, you might want to help them with some math. If the children are fairly healthy, do not currently take any monthly prescriptions, and do not regularly see a specialist, then that means they are choosing the copay plans primarily for the predictable primary care visits. If the copay plan allows them to take the children to the doctor for $35 per visit, then they are saving $53 per visit versus the HSA-qualified plan.

$88 - $35 = $53

With that information, we can compare the additional premium cost for the copay plan with the savings from the copayments. Let’s say the couple has two children and takes each of them to the doctor four times per year for sick visits. That’s eight visits between the two children.

8 x $53 = $424

If the family has to pay $100 more per month, or $1,200 per year, for the copay plan than for the HSA plan, this isn’t a good deal. By subtracting the expected savings from the additional cost, we can see that they are overpaying by $776.

$1,200 - $424 = $776

This does not even factor in the potential tax savings if the family were to go with the High Deductible Health Plan, set up a Health Savings Account, and deposit the $100 premium savings into the HSA each month. The savings would more than pay for the primary visits and could be used to pay for any prescriptions that resulted from those sick visits, and the family would save an additional $300-400 in federal taxes each year.

Obviously, each situation is different, and the math can get more complicated if your clients have specialists that they see, take prescriptions on an ongoing basis, or expect to have some costly medical tests. Still, tools like TexasHealthcareCosts.org can be helpful in explaining to your clients why it’s in their best interest to buy less insurance and use the premium savings to pay for their additional out-of-pocket expenses.